/Author%20Profile%20Caple_Claire_W.png?width=100&name=Author%20Profile%20Caple_Claire_W.png)

Business energy consumers are understandably focussed on the rocketing value of gas and electricity – and the unfortunate knock-on effect this is having on operational costs.

But the escalating cost of living is also having an impact – especially when it comes to the many non-commodity charges that make up a sizeable proportion of overall energy costs.

In his Spring Statement, Chancellor Rishi Sunak highlighted rising inflation – which is expected to reach or even exceed 7.4% by the end of this year.

Together, inflation and energy market prices are key drivers for a number of energy industry costs. This is because network costs – i.e. the charges involved in transmitting and distributing energy – are often index-linked. While system costs – i.e. those related to ensuring supply meets demand – are impacted by energy market prices.

Inflation pushing many charges up

Many industry costs rise annually with inflation. Gas transportation is a good example. Its base income is agreed in blocks of five years, with the current period running from 1 April 2021 to 31 March 2026 and set at 2018/19 prices. But each financial year, the cost is adjusted to reflect inflationary movement.

For other charges, such as Contracts for Difference (CfD), generators receive guaranteed payments for the energy they supply. But these prices are also adjusted annually to reflect inflation. This helps encourage investment in renewable generation by risk-averse investors.

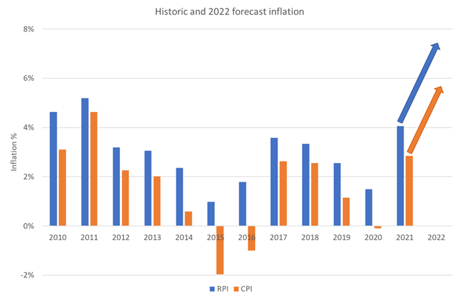

To calculate the impact of inflation on costs, some charges reference the Retail Price Index (RPI), while others track one variation or another of the Consumer Price Index (CPI).

To calculate the impact of inflation on costs, some charges reference the Retail Price Index (RPI), while others track one variation or another of the Consumer Price Index (CPI).

While these measures all monitor a large shopping basket of goods and services to calculate any change to the cost of living, the RPI includes mortgage interest payments, so is heavily influenced by house prices and interest rates.

Some energy-related costs use what’s called CPI-H, which is CPI with an added housing element, though this is accounted for differently to RPI. Both CPI and RPI run fairly parallel to each other, with RPI being higher (see graph above).

So, what does this all mean for consumers? Unsurprisingly, the non-commodity elements on energy invoices will also reflect the steep inflationary rises we are currently seeing.

Energy markets adding pressure

Some industry charges are also impacted directly by the cost of buying energy in the markets.

For example, Balancing Services Use of System (BSUoS), which recoups the cost incurred by National Grid to balance the electricity network. This ensures that supply matches demand in every part of the network, every second of every day.

A key part of this requires generators to be on standby to turn on if supply is falling short – or switch off if the grid is oversupplied.

To incentivise participation, payments have to be higher than generators could earn if they sold their supply directly on the wholesale market. So, the higher market prices are, the higher the cost of procuring balancing services.

A small upside

CfD costs are also impacted by rising energy commodity prices – but in a positive way.

CfD generators get a guaranteed price for the energy they generate, which is usually a top-up to the ‘season ahead’ or ‘day ahead’ wholesale price. However, when wholesale prices are high, this top-up payment falls – and can even become a negative.

A small ray of sunshine is that CfD costs have fallen, and in quarter 1 (Q1) 2022 were actually negative (i.e. a benefit).

As a supplier, we pass on CfD benefits to pass through customers as soon as we receive them (although this is quarterly in arrears).

The cost of losses, theft and going bust

Distribution charges include an element to cover the cost of energy loss – for example, due to gas leaks and electricity theft. And this is also impacted by high market prices.

While distribution networks have targets to minimise losses (for which they are penalised if they fail to meet), the cost is still met by consumers. And in a rising market, these loss-associated costs become more expensive.

Supplier of Last Resort (SoLR) costs are also higher. These cover the cost of new suppliers taking on the customers of suppliers who’ve gone bust.

New suppliers won’t have had an opportunity to make provision for the extra supply volume taking on these customers entails, meaning that they have to buy electricity and gas at existing market rates.

As a result, industry regulator Ofgem is allowing them to claim the difference from the current price cap for claims submitted by the end of December 2021.

This creates even more expense to be recouped from energy consumers – although SoLR costs mostly fall on domestic invoices.

So, the bottom line is that many of the non-commodity elements of energy prices are also increasing – with higher costs for consumers sadly unavoidable.

Understanding more about these elements – and the reasons for these rises – can hopefully at least make them easier to anticipate

Get to grips with non-commodity charges

Our next Energy Made Simple reports focus on network and policy-related non-commodity charges – what they are, how much they cost and what’s set to change. They are free to download and will hopefully equip you to better understand this important area of business energy costs. Register here to receive your copies.

Related Content

/npm214%20Digital_H_UB142.jpg)

Electricity costs forecast to rise every year until 2030

/npm214%20Digital_H_UB101.jpg)

Why are electricity costs increasing?

/npm214%20Digital_H_UB94.jpg)

Is your energy-buying strategy still fit for purpose?

/npm214%20Digital_H_UB146.jpg)

Why getting your energy metering right is no longer optional

The latest Market-wide Half-Hourly Settlement update

/npm214%20Digital_H_UB92.jpg)

10 things to know about the UK’s interconnector network

/npm214%20Digital_H_UB130.jpg)

How Non-Half-Hourly meters will be ‘settled’ in the new MHHS world